As of January 1st, two guidelines released by the International Sustainability Standards Board (ISSB) have been officially implemented. These guidelines are the "IFRS S1 General Requirements for Disclosure of Sustainability-related Financial Information" and the "IFRS S2 Climate-related Disclosures".

Source: IFRS official website

What kind of organization is the International Sustainability Standards Board (ISSB)?

Let's rewind to February 24, 2021, when the International Organization of Securities Commissions (IOSCO)[1] (whose members oversee over 95% of the securities markets in more than 115 jurisdictions, with the China Securities Regulatory Commission joining the organization as a formal member in 1995) issued a statement to the media, emphasizing the urgent need for globally consistent, comparable, and reliable sustainability disclosure standards. It announced its support for the establishment of the International Sustainability Standards Board (ISSB) by the International Financial Reporting Standards Foundation (IFRS Foundation).

On November 3 of the same year, during the 26th Conference of the Parties (COP26) to the United Nations Framework Convention on Climate Change, the IFRS Foundation officially announced the establishment of the International Sustainability Standards Board (ISSB), tasked with developing the International Financial Reporting Sustainability Disclosure Standards (ISSB Standards).

The development of ISSB Standards is based on existing ESG and sustainable development frameworks such as the TCFD framework, SASB standards, CDSB framework, Integrated Reporting (IR), and World Economic Forum (WEF) sustainability disclosure indicators[2]. The purpose of ISSB Standards is to provide a "global baseline" for comprehensive sustainability-related financial disclosure.

The two sets of standards already issued (IFRS S1 and S2) differ in that the former is a general requirements standard, while the latter focuses on climate-related disclosure requirements. Each category of standards will cover governance, strategy, risk management, as well as indicators and targets.

For businesses, the focus is on the "Scope 3" disclosure mentioned in IFRS S2. Previously, while disclosing sustainability-related information, Scope 1 and Scope 2 were mandatory disclosures, and Scope 3 was optional (recommended but not required).

However, the new ISSB standards explicitly require companies using ISSB standards to disclose Scope 3 data (with explanations required if unable to disclose), shifting Scope 3 disclosure from voluntary to mandatory. Therefore, businesses should recognize the importance of ensuring proper Scope 3 disclosure.

Source: [Draft] IFRS S2 Climate-related Disclosures, P41

PART.01 The starting gun for scope 3 disclosure has been fired: while companies have buffer time, early preparation is advisable

Due to the numerous challenges companies face in carbon emission collection and data accuracy, IFRS S2 provides transitional relief provisions. These provisions allow companies to not disclose Scope 3 greenhouse gas emissions in the first year of applying the standard. Instead, emissions for the current year (Scope 1, Scope 2, and Scope 3) can be disclosed in the second year.

Transitioning from "recommended disclosure" to "mandatory disclosure", what is the binding nature of ISSB standards on companies? Can companies be exempted from disclosure responsibility on grounds of "impracticality"? The answer is almost impossible.

A report by Ernst & Young [3] mentions that the measurement framework for Scope 3 greenhouse gas emissions provided by IFRS S2 allows for a wide range of data sources for companies, including the use of estimates based on third-party information (such as industry averages). At the same time, it sets a high threshold for what constitutes "impracticability," stating that this requirement is only impracticable if a company has made all reasonable efforts and still cannot comply. It is anticipated that very few companies will be able to utilize this exemption in practice.

Which enterprises will be significantly impacted by the ISSB standards?

The International Organization of Securities Commissions (IOSCO) announced its recognition of the ISSB standards at the end of July 2023 and called on its 130 member jurisdictions to consider incorporating them into their respective regulatory frameworks. While the China Securities Regulatory Commission is a member of IOSCO, A-shares in China have not officially adopted the ISSB standards yet.

Domestically, the Hong Kong Stock Exchange introduced new climate-related disclosure requirements based on the ISSB's climate-related disclosure standards in April 2023, moving climate-related disclosure from a "comply or explain" approach to mandatory disclosure.

It's worth mentioning that there are a total of 149 A+H listed companies (companies listed on both the Shanghai or Shenzhen Stock Exchange and the Hong Kong Stock Exchange) in China. These well-known domestic enterprises need to comply with the ISSB standards when disclosing sustainable information.

Internationally, many countries have actively responded to or implemented the ISSB standards. For example, in July 2022, the Singapore Sustainability Reporting Advisory Committee (SRAC) plans to require all listed companies to disclose climate-related information according to the new ISSB standards from the 2025 financial year onwards. Additionally, countries such as Canada, the UK, Japan, South Korea, Australia, Brazil, and Nigeria are planning or preparing to adopt the ISSB standards.

Hua Jingdong, Vice Chairman of the ISSB, publicly stated regarding the implementation of IFRS S1 and IFRS S2 standards: "We do not pursue perfection, but the start." Achieving sustainable information disclosure under a unified framework is challenging due to differences in data foundations and disclosure standards. However, enterprises should be aware that climate-related sustainable information disclosure is the trend, and they should complete the disclosure of Scope 3 data as early as possible.

PART.02 Why is "Scope 3" so important?

First, let's understand what "Scope 3" refers to.

The definition of Scope 3 originates from the Greenhouse Gas Protocol developed by the World Resources Institute (WRI) and the World Business Council for Sustainable Development (WBCSD). Scope 3, along with Scope 1 and Scope 2, constitutes the three domains of greenhouse gas accounting.

Source: GHG protocol-A Corporate Accounting and Reporting Standard (revised edition)

Scope 1 refers to direct greenhouse gas emissions from sources owned or controlled by the reporting entity, while Scope 2 refers to indirect greenhouse gas emissions from the purchased energy.

Scope 3 encompasses all other indirect greenhouse gas emissions occurring along the value chain of the reporting entity that are not covered by Scope 2 emissions, including both upstream and downstream emissions. Scope 3 emissions are categorized into fifteen categories, with eight categories representing upstream emissions and the remaining seven categories representing downstream emissions of the reporting entity.

Source:HSBC

Why is Scope 3 important?

Compared to Scope 1 and Scope 2 emissions of a company, upstream and downstream emissions are often larger (or perceived to be larger)[4].

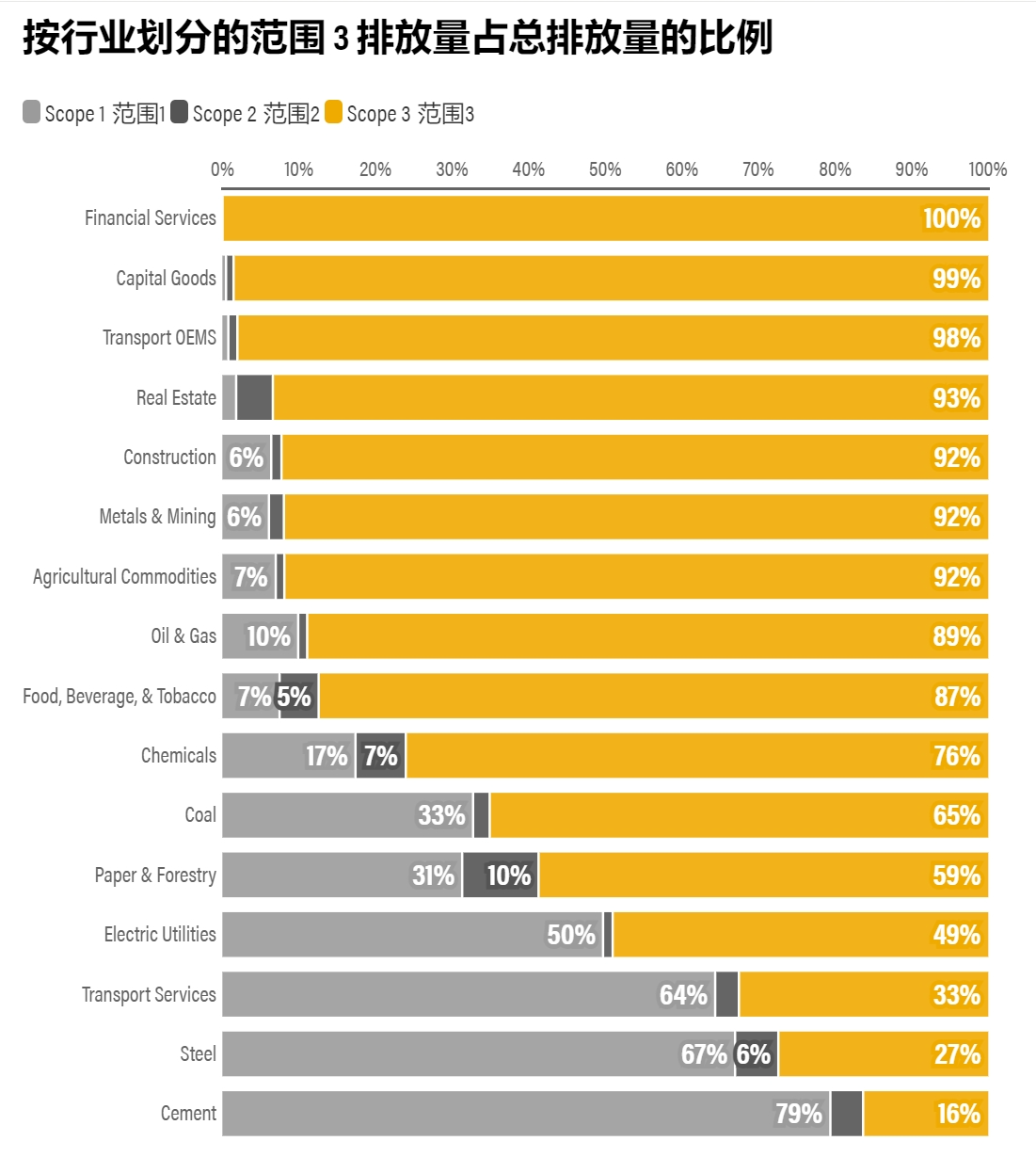

Source:WRI

According to estimates from the CDP (formerly the Carbon Disclosure Project), Scope 3 emissions on average represent 75% of a company's total emissions. The proportion of Scope 3 emissions to total emissions varies across different industries. Industries such as financial services, capital goods, and transportation manufacturing have Scope 3 emissions that make up 100% or close to 100% of their total emissions. Additionally, in industries such as real estate, construction, metals and mining, and agriculture, Scope 3 emissions account for over 90% of total emissions. This highlights that for most companies, Scope 3 emissions constitute a significant portion of their overall carbon footprint along the value chain, while for certain industries like steel, cement, and transportation services, Scope 1 emissions play a larger role in the overall carbon footprint.

Source: Net-Zero Challenge:The supply chain opportunity,WEF&BCG

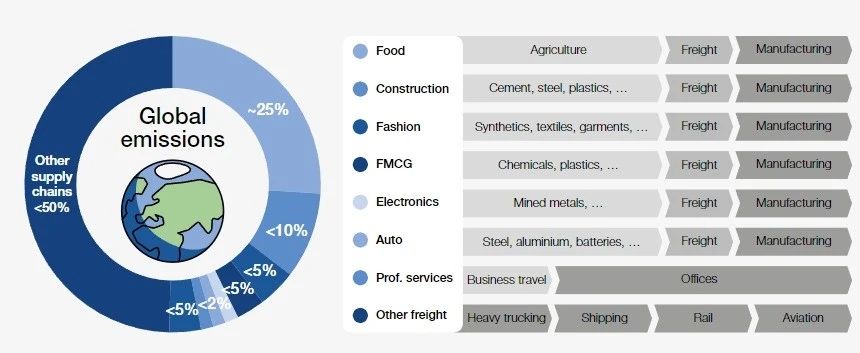

Another study [5] also indicates that in the electronics, construction, automotive, food, fashion, and fast-moving consumer goods industries, Scope 3 emissions account for 77%, 81%, 82%, 83%, 85%, and 90% of total product carbon emissions, respectively, all exceeding 75%.

Although accounting for Scope 3 emissions is crucial for companies, they face numerous challenges in the actual process of calculating carbon emissions, including the large workload, relatively weak accounting foundations (such as lack of original data), and the inability to control the behavior of value chain partners.

Scope 3 accounting and emission reduction efforts often involve multiple industries and domains, requiring collaboration among various stakeholders. It is crucial for companies to collaborate with key upstream stakeholders, particularly suppliers, in addressing Scope 3 emissions (collaborative supply chain decarbonization). Nigel Topping, the UN High-Level Climate Champion, once mentioned, "Decarbonizing the supply chain will be a game-changer for corporate climate action".

PART.03 Decarbonizing the supply chain is challenging.

The carbon emissions along the supply chain are much higher than you might imagine. The eight supply chains, from raw materials to final product manufacturing, account for over half of the global greenhouse gas emissions, including food, construction, fashion, fast-moving consumer goods, electronics, automotive, professional services, and freight.

Source:Net-Zero Challenge:The supply chain opportunity,WEF&BCG

Why is decarbonizing the supply chain challenging?

Enterprises lack visibility into one of the largest sources of emissions, primarily from their upstream suppliers, preventing them from accelerating emission reduction, enhancing supply chain sustainability, and reducing overall carbon footprint effectively.

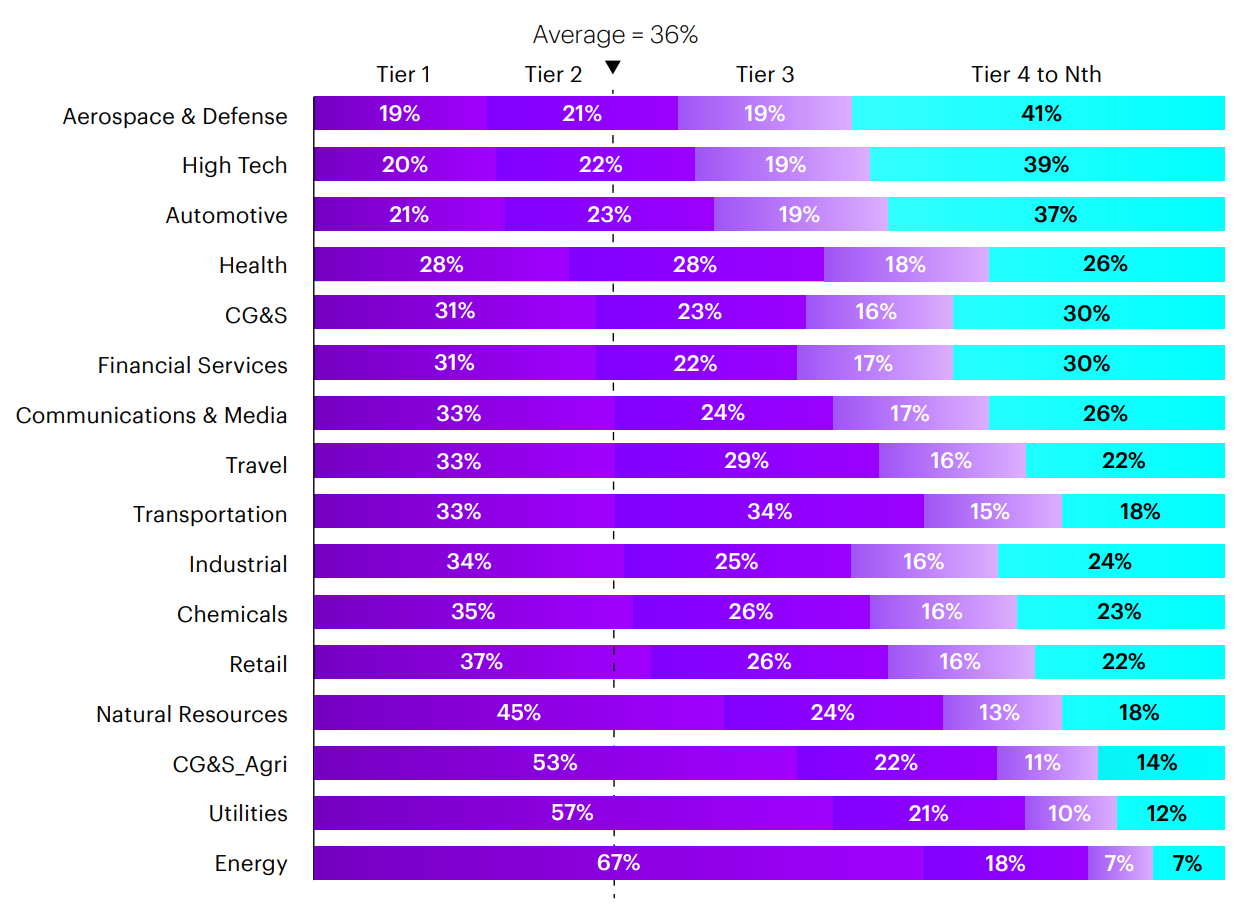

In many companies, emissions are widely dispersed across the enterprise and n-tier suppliers (including suppliers and their suppliers), with most Scope 3 emissions generated by Tier 2+ suppliers. A study by Accenture found that emissions beyond Tier 1 suppliers exceeded those of Tier 1 across most industries. On average, Tier 1 suppliers accounted for only 36% of total upstream emissions. In industries like aerospace and defense, high tech, and automotive, around 80% of upstream emissions come from beyond Tier 1 suppliers.

Source:Accenture

In industries with less complex supplier networks, a significant portion of emissions comes from Tier 1 suppliers. These industries include energy, utilities, agricultural consumer goods and services, and natural resources. Conversely, aerospace and defense, high tech, and automotive industries have relatively complex upstream emissions. In most cases, these emissions often occur deeper within a company's supplier network.

In some scenarios, a large enterprise may have over 20,000 direct Tier 1 suppliers covering more than 50 cost categories and spanning different countries globally. Additionally, each of these suppliers may have hundreds or even thousands of their own Tier 2 suppliers, and so forth.

For complex supply chain networks, it's crucial to establish mechanisms for higher transparency at the supplier level, followed by collaboration with suppliers contributing significantly to emissions to reduce carbon emissions.

Supply chain management relies heavily on the empowerment of digital technologies. This primarily includes two aspects: enterprise-side digital systems, such as carbon reduction progress management, carbon emission dashboards, and product life cycle assessment (LCA) data design; and supplier-side digital platforms, including supplier carbon reduction progress tracking, carbon reduction proposal initiatives, carbon emission data management, and support systems.

Carbon Balance Technology utilizes digital technologies such as blockchain, big data, and IoT to help enterprises with complex supply chains build highly transparent supply chain carbon reduction management platforms. These platforms offer "one-touch access" and strict traceability, providing end-to-end supply chain carbon reduction services, and enabling one-stop management of multi-tier suppliers. Additionally, the platform prioritizes technological confidentiality and data security, ensuring that circulated carbon data undergoes third-party verification to prevent the leakage of sensitive supplier data and safeguard the compliance and security of critical enterprise data.

References

[1]国际证监会组织,百度百科词条

[2]中国企业需及时洞悉ISSB可持续性信息披露准则的细则要求,普华永道

[3]IFRS S2的核心内容之指标和目标:范围三排放——ISSB准则深入解读系列文章之七,安永

[4]GHG. A Corporate Accounting and Reporting Standard REVISED EDITION

[5]Net-Zero Challenge: The supply chain opportunity,WEF&BCG

[6]Thought you knewthe Scope 3issues in yoursupplv chain?,Accenture