In recent years, global attention to climate change has been increasing. Regulatory scrutiny, supervision, and policy support from governments, emissions reduction pressure from stakeholders such as consumers and investors, as well as intrinsic development needs of businesses, are driving automotive companies towards a direction that is more carbon-efficient, environmentally friendly, and sustainable. The automotive industry is transitioning towards electrification and cleaner fuel sources, with major automakers setting net-zero emission goals. Carbon emission management is becoming a crucial tool for automotive companies and industry chain suppliers to achieve carbon neutrality and net-zero emissions.

01 The Global Automotive Industry Moving Towards Carbon Neutrality

As a pillar industry of the national economy, China's automotive industry has been the world's largest for 14 consecutive years. The vehicle fleet exceeds 300 million, ranking first globally, and car exports have surpassed Japan, making China the world's top exporter. While the new energy vehicle sector in China is gradually becoming a global leader, the rapid development of the automotive industry has also brought significant pressure for carbon emission reduction.

According to statistics, emissions from global road transportation account for 11.9%[1] of total carbon emissions, with 60% from passenger travel and 40% from road freight[2]. In 2022, carbon emissions from the operation of vehicles in China accounted for about 8% of the total societal carbon emissions and 80% of the transportation sector[3].

In recent years, major economies worldwide have successively released visions for carbon neutrality. Over 150 countries globally have proposed carbon neutrality goals, with more than 20 countries and regions setting comprehensive electrification targets for automobiles. Green and low-carbon initiatives have become the common choice for the global automotive industry in its journey towards carbon neutrality.

Under the "dual-carbon" goals, green and low-carbon development has become an intrinsic requirement for the high-quality development of China's automotive industry. The "14th Five-Year Plan for Circular Economy Development" lists the promotion of "full lifecycle management of automobiles" as one of the six key actions from 2021 to 2025. The "Action Plan for Carbon Peak by 2030" proposes that by 2030, the proportion of new energy clean power in transportation should reach around 40%. Therefore, accelerating the green and low-carbon transformation of the automotive industry is not only a crucial support for implementing the national "dual-carbon" strategy but also an inherent requirement for the high-quality development of the industry.

The automotive industry has characteristics such as a long industrial chain, wide coverage, and extensive connections with various related industries. Apart from its own production chain, it is highly associated with mining, manufacturing, energy production and supply, transportation, and other industries. Therefore, the decarbonization of the automotive industry can also drive the low-carbon transformation of related industries, making it a crucial battleground for China's dual-carbon transformation.

02 Three Steps for Low-Carbon Transformation of Automotive Enterprises and Examples

Moving towards carbon neutrality, automotive companies can achieve low-carbon transformation in three steps: commitment, action, and tracking reporting.

Commit:Formulate a carbon-neutral development strategy and make carbon-neutral commitments. Establish and transition to a sustainable new development model by integrating carbon-neutral goals into the company's development strategy. Evaluate the current status and potential for decarbonization, formulate scientifically based carbon goals (such as SBTi), and develop a roadmap for carbon neutrality.

Nowadays, more and more companies are incorporating ESG performance into their decision-making processes, and low-carbon development is one of the important indicators to measure their environmental (E) performance. Therefore, formulating a company development strategy guided by carbon neutrality can achieve the alignment of environmental value and business value. As shown in the chart below, companies such as BMW, Audi, Mercedes-Benz, Volkswagen, BYD, Geely, and others have set emission reduction targets.

Source:2030 Sustainable Development White Paper for the Automotive Industry

BMW Group is committed to achieving carbon neutrality by 2050 and has outlined a clear roadmap for decarbonization to meet this goal. In addition to focusing on its own operational scope, the company also addresses the entire value chain. It takes steps to reduce emissions across various stages, including production, supply chain, product usage, logistics, dealerships, non-production sites, and other areas.

Source:BMW Group China Sustainable Development Report 2022

Geely Holding Group has committed to achieving carbon neutrality in its own operational aspects no later than 2040. The group has also set carbon reduction targets for each of its brands. Volvo, a brand under Geely, plans to make all new models fully electric by 2030. The ambitious plan of achieving climate neutrality by 2040 has been approved by SBTi.

Source:Geely Holding Group 2022 Sustainable Development Report

Act:Implementing carbon neutrality commitments. From commitment to results, action is the only solution. Many automotive companies focus on using clean energy, improving materials and processes, green supply chain management, low-carbon operations, carbon offsetting, and other initiatives.

For example, Mercedes-Benz has introduced the "2039 Vision" and accelerated the transition to "fully electric." They have taken measures in product development, supply chain, production processes, vehicle operations, and recycling and waste disposal. In 2023, they partnered with Baosteel to apply low-carbon aluminum in automotive products to reduce the carbon footprint. They have also formulated a battery lifecycle management strategy, implemented digital technology for end-to-end battery traceability, and initiated sustainable financing projects, among other actions.

Source:Mercedes-Benz Group - China Sustainable Development Blue Book 2022-2023

Track & Disclose:Tracking low-carbon development performance and disclosing reports. Scientifically accounting for corporate carbon emissions and quantifying assessments, regularly tracking low-carbon development performance, and disclosing reports. Based on compliance with policies (such as environmental disclosure requirements) and trade regulations (such as CBAM and new battery laws), presenting the latest progress to stakeholders and establishing a responsible corporate image.

As shown in the chart below, Geely Holding Group disclosed carbon emission data for its Scope 1, 2, and 3 in its 2022 Sustainable Development Report.

Source:Geely Holding Group 2022 Sustainable Development Report

In its 2022 Sustainable Development Report for China, BMW Group disclosed carbon emission data for scopes 1, 2, and 3, along with a distribution map of the carbon footprint for 2022. In scope 3, the product usage phase contributes to over 75% of carbon emissions. BMW is addressing this by expanding charging infrastructure and offering green charging services to reduce carbon emissions generated during the usage phase of BMW vehicles.

Source:BMW Group China Sustainable Development Report 2022

Whether it's a carbon footprint check for a single vehicle or a corporate-level carbon emission inventory, the low-carbon transformation of automotive companies requires carbon emission data as a foundational support. To conduct supply chain carbon emission management, it is necessary to trace back to the upstream or even more distant energy supply or raw material extraction.

03 Differences in carbon management focus between Internal combustion engine vehicles and new energy vehicles

The basic life cycle stages of conventional and new energy vehicles are the same, including material production, vehicle manufacturing, vehicle use, and recycling.

The difference lies in that the carbon emissions from traditional internal combustion engine vehicles are mainly concentrated in the usage phase (accounting for about 80%), while the carbon emissions from material (component manufacturing) and vehicle manufacturing stages only contribute to 20%[4]. With the widespread adoption of new energy vehicles, the primary source of carbon emissions is expected to transition from the usage phase to the production phase. The proportion of carbon emissions from materials and manufacturing stages, especially in battery production, may rise from the current 20% to 85%[5].

Therefore, carbon emission management for conventional vehicles focuses on the usage phase, while carbon emission management for new energy vehicles pays more attention to the production phase, particularly in the battery production process.

04 How to determine the scope of carbon emission accounting?

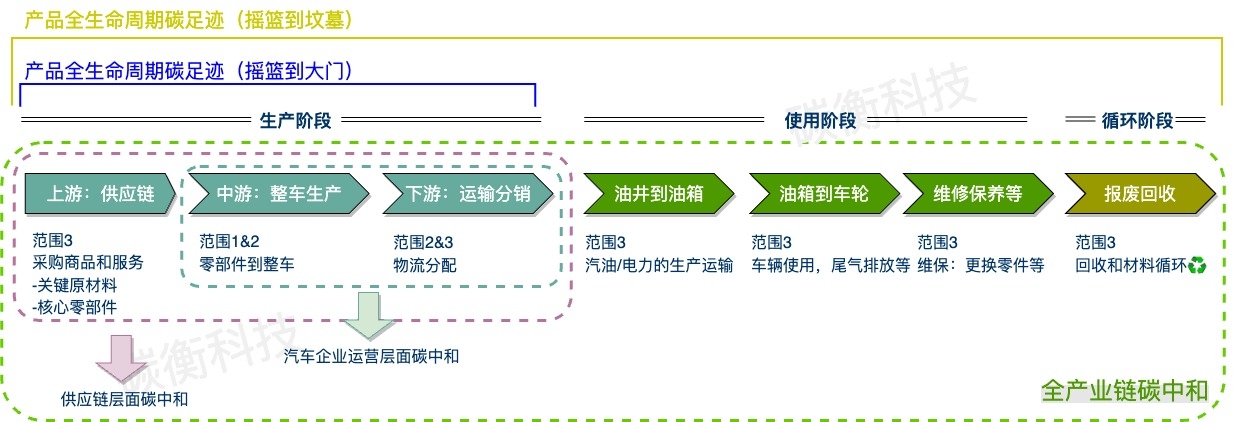

From the traditional lifecycle perspective of "production-usage-end-of-life recycling" for automobiles, it can be divided into fuel cycle and material cycle. Specifically, the fuel cycle includes the acquisition phase (including processes such as the extraction, transport, and production transport distribution of primary energy) and the operational phase (the fuel consumption process during the vehicle's operation). The material cycle involves the extraction and transport of raw materials, production and processing of vehicle materials, manufacturing of whole vehicles and components, as well as the process of component replacement and recycling after the end-of-life disposal of the vehicle.

As shown in the above figure, the carbon emissions throughout the lifecycle of automotive products involve various industries, such as mining, manufacturing, energy supply, and transportation. With global efforts to address climate change and the implementation of China's "Dual Carbon" strategy, the momentum has shifted towards the electrification transformation centered around new energy vehicles and the low-carbon transformation of traditional energy power systems centered around internal combustion engines. The integration between the new energy-related industries and the automotive industry has become closer.

Combining the two figures above and considering it from the perspective of corporate carbon emissions, the carbon emission boundaries at the organizational operational level for automotive companies like BMW, Volkswagen, etc., typically include carbon emissions generated from activities such as car assembly manufacturing and overall vehicle distribution operations. On the supply chain level, carbon emissions also encompass the procurement of key raw materials and core components, bringing goods or services from upstream suppliers. At the entire industry chain level, carbon emissions need to account for the vehicle usage stage and the end-of-life recycling and reuse stage. Correspondingly, to achieve carbon neutrality at the organizational, supply chain, and entire industry chain levels, efforts are required to reduce and offset carbon emissions generated at each stage and in each process.

From the perspective of the entire lifecycle carbon emissions of a car product, to account for the car's carbon footprint from "cradle to grave," it is necessary to consider not only 1) the car assembly production and transportation distribution processes but also 2) the upstream production of core components and the production processes of key raw materials that extend further upstream. Additionally, it should encompass 3) the carbon emissions generated during the production, distribution, and usage of the fuel/energy used during the car's operational stage. Furthermore, it should include 4) the carbon emissions generated during the disassembly and recycling process of the car.

05 Conclusion

Although many automotive companies have set emission reduction targets or climate ambitions, most of them have only committed to "carbon neutrality" at the level of their own operations, and the path to carbon neutrality for the supply chain and the entire industry chain is still long.

Currently, the carbon accounting methods and data collection for the value chain of domestic automotive companies are relatively weak. Most companies calculate the carbon footprint of vehicles by matching material weight information from the bill of materials (BOM) with corresponding material background data. However, automobiles are composed of a large number of components, with each component having multiple suppliers. The accuracy and granularity of data provided by suppliers vary, and there are significant challenges in coordinating and managing carbon data across the industry chain.

For the complex lifecycle of automobiles, determining, monitoring, and tracing the carbon footprint information of both whole car enterprises and supply chain enterprises, coordinating carbon data management across the industry chain, and updating factor libraries in a timely manner to meet supervision, regulatory requirements, and compliance disclosure of carbon information are challenges faced by the entire automotive industry chain.

In the future, in-depth articles on the automotive industry will bring you more industry solutions.

References

[1] https://ourworldindata.org/ghg-emissions-by-sector

[2]https://www.iea.org/data-and-statistics/charts/transport-sector-co2-emissions-by-mode-in-the-sustainable-development-scenario-2000-2030

[3] 汽车产业绿色低碳发展路线图1.0

[4] https://sports.sohu.com/a/743724639_121119176

[5] https://www.mckinsey.com.cn/从电动化到供应链,中国车企脱碳的必由之路/